Inflation sends mixed signals: manageable for the Federal Reserve, painful for consumers

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

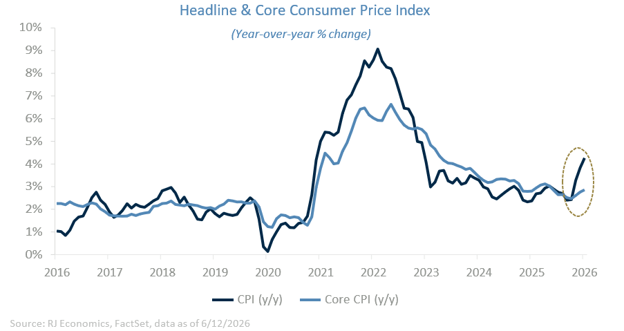

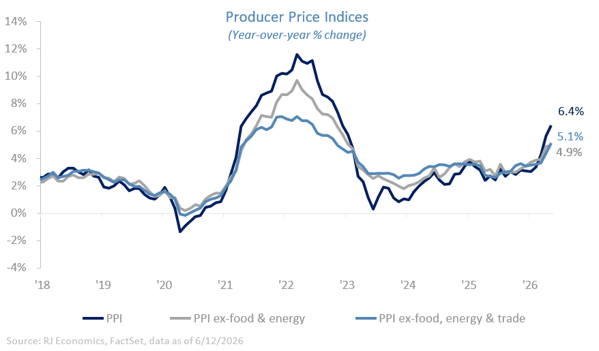

This week’s inflation data highlights a growing disconnect between how markets interpret inflation and how consumers experience it. The May Consumer Price Index (CPI) report delivered a nuanced message: While headline inflation accelerated, core inflation remained relatively contained, an outcome that provides some comfort to policymakers. In contrast, the Producer Price Index (PPI) data raised more concern, signaling that upstream price pressures are building and could feed into future consumer inflation.

From a market perspective, the CPI report leans constructive. Relatively contained core inflation suggests that underlying price pressures are not spiraling, supporting the view that monetary policy is on the right track. However, the PPI report tempers that optimism, pointing to risks that inflationary pressures could re-emerge in coming months.

For consumers, the story is far less encouraging. Inflation rose to its highest level since April 2023, reinforcing the perception that the cost of living remains elevated. This helps explain persistently weak readings in consumer sentiment and confidence surveys.

The divergence in perspectives comes down to what each group is measuring. Markets and policymakers focus on the trajectory of inflation, whether it is moving higher or lower. Consumers focus on the absolute price level. Even if inflation moderates, prices remain significantly above pre-pandemic levels, and that gap continues to weigh on household finances.

Businesses also sit at the intersection of these dynamics. While they benefit from stable and predictable inflation, unexpected shifts – such as those suggested by the recent PPI report – can disrupt planning and pressure margins. Rising input costs, if sustained, may eventually be passed through to consumers, prolonging the inflation cycle.

Central banks aim to maintain low and stable inflation, not zero inflation. The Federal Reserve’s 2.0% long-term target remains the anchor for policy and expectations. Importantly, markets are less sensitive to the exact level of inflation and more focused on its stability and predictability. It is volatility and surprises – not modestly higher inflation – that create the greatest economic disruption.

This is why inflation expectations remain a critical variable. As long as longer-term expectations stay well anchored, the Fed retains flexibility. However, any signs of expectations becoming unmoored would significantly alter the policy outlook.

Bottom line

The latest data reinforces a key theme for markets: Inflation progress is uneven. Core CPI supports a cautiously constructive outlook for policy, but rising PPI introduces upside risks to inflation. For consumers and businesses, the near-term reality remains challenging, with elevated price levels and potential cost pressures still firmly in place.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.