Crude awakening: The Iran conflict’s aftereffects will linger long after it’s over

Raymond James Senior Investment Strategist Pavel Molchanov examines the longer-term ripple effects of the US-Iran conflict

Every major geopolitical crisis has two types of effects: those that occur during the crisis itself and those that remain on a long-term basis, perhaps even permanently. The US-Iran conflict is no exception. The most severe oil supply disruption in world history – and related impacts on liquefied natural gas, helium, ammonia and aluminum – has led to higher commodity prices around the world, with some countries experiencing outright shortages.

While $100+/barrel oil and $4.00+/gallon gasoline are already in the rearview mirror, some of the aftereffects of this unprecedented crisis are here to stay. Just as the energy shocks of the 1970s led to, among other things, the creation of emergency oil stockpiles and a shift away from gas-guzzling vehicles, the latest crisis may exert influence on policymakers, businesses and consumers for years or even decades to come.

Natural gas stockpiling: A long-missing piece of the energy security puzzle

When the 32 member countries of the International Energy Agency (IEA) pledged this past March to release 400 million barrels from their emergency oil stockpiles, it was by far the largest such action in the IEA’s 52-year history. In fact, it was larger than all previous ones combined. But the IEA’s remit has never been extended to include natural gas. In retrospect, that was a big oversight, dating back to the IEA’s creation in 1974.

Natural gas plays a much greater role in the global energy mix today than it did half a century ago. Whereas oil is overwhelmingly used for transportation, natural gas has a wide range of use cases: electric power, heating, industrial processes (e.g., steel mills) and the chemical industry (where it has been increasingly displacing oil). And while global oil demand has been growing at less than 1% per year in the post-COVID era – even setting aside the decline in 2026 due to the price spike – global natural gas demand tends to increase two to three times faster.

Europe’s energy crisis in 2022 – the result of Russia’s decision to cut off natural gas supply after its invasion of Ukraine – illustrated that natural gas also needs to be stockpiled. Europe has made progress in that regard over the past four years. By contrast, countries in Asia – the main importers of liquefied natural gas from Qatar, whose main facility was seriously damaged by an Iranian strike in March – have yet to follow suit. Along the same lines, there may be efforts to stockpile natural gas derivatives such as ammonia (a key input for fertilizer) and helium (playing an important role in semiconductor manufacturing).

More renewables and nuclear power: a wake-up call for Asian economies

Countries such as Japan and South Korea, which are virtually 100% dependent on imported oil and natural gas, cannot drill their way toward energy independence – they simply do not have the required natural resources. What they are able to do, however, is shift their electricity mix towards renewables – wind, solar and, in certain cases, hydro and geothermal – as well as nuclear power. Whereas power plants that burn fossil fuels require nonstop supply of those raw materials and thus are prone to supply disruptions, energy security can be enhanced by shifting to electricity sources that face little to no geopolitical risk.

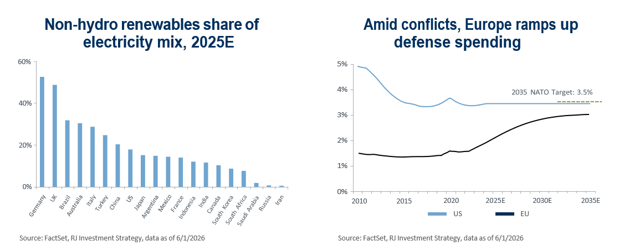

The energy crisis of 2022 provided an impetus for European countries to accelerate the buildout of renewable power generation, as well as nuclear (with the notable exception of Germany), and this latest crisis may provide a similar wake-up call for countries in Asia. As shown in the chart above, Germany and the UK are among the leaders in non-hydro renewable power as a percentage of the electricity mix.

China and Japan are further behind – although China is installing more solar and wind in absolute terms than the rest of the world combined – with India and South Korea near the bottom of the international spectrum. Wind turbines, solar panels and other products for the electric grid are manufactured by companies in the industrials sector, and bolstered demand for this equipment would support our positive stance on the sector.

Faster EV adoption: A step that consumers can take to protect themselves

The 50% run-up in US retail gasoline prices during the Iran conflict provided the latest illustration of the fact that when oil prices rise, they rise worldwide – even in countries such as the US that are net exporters. The global nature of the oil market means that there is no such thing as immunity from oil price hikes. A similar story played out during the 2022 energy crisis, even though Russian oil exports (in contrast to natural gas) never actually experienced a significant disruption.

The good news is that consumers and businesses can protect themselves from sudden spikes in oil prices by shifting toward electric vehicles (EVs). (Electricity prices are rising over time, but because they are regulated, they are not prone to abrupt changes in either direction.) With the exception of China, the price tag of EVs tends to be higher than comparable conventional vehicles, but the higher fuel prices become, the shorter the payback period.

If, hypothetically, gasoline were to stay at $4.00 per gallon permanently, we estimate that the payback for US consumers would be in the range of six to seven years, as compared to eight to 10 years if prices were back to the $3.00 per gallon level.

As it stands, EVs comprise more than half of new auto sales in China, roughly 30% in Europe, but only roughly 10% in the US. Interestingly, among the leaders in EV adoption are low-income countries with essentially no oil of their own – Ethiopia and Nepal are notable case studies – because it is precisely these countries that struggle the most during oil shocks. The faster EV adoption progresses, the slower global oil demand is set to grow in the future, which is among the reasons for our underweight on the energy sector.

It is worth noting that EVs, more so than conventional vehicles, depend on critical minerals such as lithium and nickel (for batteries) and rare earths (for powertrains). The Iran conflict directly disrupted supply of only one metal – aluminum, which is refined in the UAE and Bahrain, though there are hypothetical geopolitical scenarios that could have far-reaching impacts on critical minerals. Case in point: war between China and Taiwan.

But here’s the essential difference between critical minerals and oil: While disruption of such exports from China would make it more difficult to manufacture new EVs, it would have no effect on existing EV drivers. By contrast, every owner of a conventional vehicle felt the impact of $100+ oil each time they pulled up to the fuel station.

More defense spending: In a volatile world, past isn’t always prologue

Never in the modern history of the Middle East has there been a war that embroiled more countries than this one. The first Gulf War in 1991 involved many countries in the region, but Iran chose to stay off to the side. More recently, brief conflicts between Israel and Iran remained limited to just those two countries. But in March and April of this year, Iran’s willingness to attack fellow Muslim countries around the Persian Gulf shocked its neighbors. While air defenses in these countries were partially successful in intercepting Iranian missiles and drones, there was still widespread damage to infrastructure, including, as mentioned earlier, energy facilities. It is a good bet that governments across the region will want to be even better prepared in the future.

Looking beyond the Middle East, this conflict had a second-order effect: It provided a hefty boost to the Russian economy. Accordingly, the Kremlin will have even more resources to continue its war in Ukraine. As NATO’s European members ramp up defense spending toward the alliance’s official target of 3.5% of gross domestic product by 2035, the threat from Russia is top of mind. While we doubt that Europe as a whole will average 3.5%, those countries that are geographically closer to Russia – Baltic states, Poland, to some extent Germany – have a heightened perception of risk and therefore are willing to spend more. Growth in defense spending among the US and its allies is also a driver of our overweight on industrials.

Bottom line

As was the case with previous geopolitical crises, we expect the Iran conflict to have a series of long-term consequences. Given that energy was more affected by this conflict than any other sector of the global economy, these aftereffects are disproportionately energy-related: stockpiling of natural gas, a push for energy security via renewable and nuclear power and bolstered demand for electric vehicles.

Looking beyond energy, higher defense spending is also likely. The ways in which these aftereffects materialize will vary in different parts of the world. For investors, the key message is that all long-term trends carry opportunities as well as risks.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results.

Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.